IRS-Qualified Estate Tax Valuations for High-Net-Worth Estates in Palo Alto, CA

IRS-Qualified Estate Tax Valuations for High-Net-Worth Estates in Palo Alto, CA

Settling an estate for a high-net-worth individual requires meticulous financial precision, especially when prime real estate assets form the cornerstone of the portfolio. In Palo Alto, located in Santa Clara County at the heart of Silicon Valley, residential properties consistently rank among the most valuable nationwide. For estate attorneys, wealth advisors, corporate trustees, and surviving family members, securing an IRS-qualified estate tax appraisal is an essential safeguard. A certified valuation protects against tax compliance exposure, establishes an accurate cost basis for heirs, and fulfills fiduciary duties under California and federal law.

Pacific Appraisers delivers independent estate tax appraisals crafted specifically for the Silicon Valley luxury market. Whether valuing a historic Craftsman in Old Palo Alto, a modern architectural home in Crescent Park, or a sprawling estate in University South, our comprehensive appraisal reports comply strictly with the Internal Revenue Service and the Uniform Standards of Professional Appraisal Practice (USPAP).

Understanding the Micro-Markets of Palo Alto Real Estate

Palo Alto features distinct micro-neighborhoods where property values vary dramatically based on lot utility, architectural significance, and historical designations. A broad citywide average fails to capture these hyper-local dynamics.

Neighborhoods like Old Palo Alto and Crescent Park feature multi-million-dollar estates on expansive, oak-canopied lots. In contrast, areas such as Midtown Palo Alto or College Terrace reflect different density rules, historic overlay zones, and building coverage limits.

When conducting a date of death appraisal or estate valuation in Palo Alto, CA, appraisers must analyze specific micro-market drivers:

-

Zoning and Lot Coverage Caps: Palo Alto strictly regulates lot coverage, total floor area ratios (FAR), and basement regulations. Land utility directly governs property value.

-

Historic Preservation Overlays: Properties designated under Palo Alto

-

Historic Inventory ranks face strict alteration guidelines, impacting both functional utility and valuation adjustments.

-

Proximity to Key Corridors: Location factors, such as proximity to Stanford University, Downtown North, or quiet residential cul-de-sacs, create measurable value differentials.

-

Custom Construction and Smart Home Systems: Modern Silicon Valley tech builds feature high-end automation, green building tech, and custom structural elements that demand detailed paired-sales analysis.

The Valuation Issue: Why Automated Models and Standard Appraisals Fall Short

Under Treasury Regulation § 20.2031-1, fair market value for federal estate tax purposes represents the price at which property would change hands between a willing buyer and a willing seller, neither being under compulsion and both possessing reasonable knowledge of relevant facts. This valuation must reflect market conditions on the specific date of death or the alternate valuation date six months later.

In high-value Silicon Valley zip codes like 94301 and 94306, generic appraisal methods and online estimates fail entirely:

-

Automated Valuation Models (AVMs) Ignore Custom Features: Computer algorithms evaluate basic metrics like square footage and bedroom count. They cannot evaluate a multi-million-dollar custom renovation, high-end interior finishes, or custom basement living quarters.

-

Standard Mortgage Appraisals Lack IRS Defensibility: Lenders use appraisals designed for underwriting risk, which differ significantly from the rigorous standards required for IRS Form 706 tax filings.

-

Flawed Historical Reconstruction: Retrospective estate tax valuations require analyzing historical market conditions active on the date of death. Generic software cannot accurately reconstruct historical market sentiment or micro-neighborhood comparable data.

Fiduciaries relying on unverified estimates risk severe administrative delays, audit notices, and financial penalties from state and federal tax authorities.

Legal and Financial Implications for Estate Fiduciaries

When filing IRS Form 706 for high-net-

worth estates, valuation accuracy directly dictates tax exposure. Under Internal Revenue Code (IRC) § 6662, incorrect property reporting results in strict statutory penalties:

-

Substantial Valuation Understatement: If the reported value is 65 percent or less than the correct value established by the IRS, a 20 percent penalty applies to the underpaid tax amount.

-

Gross Valuation Understatement: If the reported value is 40 percent or less than the true market value, the tax penalty increases to 40 percent.

At the same time, understating value hurts heirs when inheriting real estate. Under IRC § 1014, beneficiaries receive a “stepped-up” basis equal to the property fair market value on the decedent’s date of death. Establishing an accurate, fully defensible valuation minimizes capital gains taxes when the heirs eventually sell the property while shielding the estate from current IRS audit liability.

An IRS Qualified Appraisal must be executed by an IRS Qualified Appraiser who holds recognized state certification, regular professional education, and demonstrable experience valuing luxury real estate in the subject market.

The Pacific Appraisers Approach: Technical Accuracy and Local Expertise

Pacific Appraisers approaches complex real estate valuations across Santa Clara County with rigorous technical standards and complete independence. Our methodology ensures that every report withstands review by probate judges, estate attorneys, wealth managers, and IRS auditors.

1. Rigorous On-Site Physical Inspection

Our certified appraisers perform detailed physical inspections, documenting architectural features, structural condition, quality of finishes, floor plan functionality, and auxiliary structures like accessory dwelling units (ADUs) or pool houses.

2. Hyper-Local Market Analysis

We examine comparable sales within specific Palo Alto micro-neighborhoods rather than relying on broad citywide statistics. Quantitative adjustments are applied for lot square footage, zoning restrictions, view corridors, and high-end luxury improvements.

3. Precision Retrospective Valuations

For date of death assignments, our appraisers reconstruct the historical market landscape back to the target date. We verify historical MLS records, public land transactions, economic conditions, and prevailing interest rates active at that exact time.

4. Complete USPAP Compliance and Unbiased Objectivity

Every appraisal produced by Pacific Appraisers adheres strictly to USPAP standards and federal tax requirements. As an independent third-party valuation firm, our reports provide clear, objective, and fully supported conclusions.

Secure Your Estate Assets with Certified Silicon Valley Appraisers

Managing an estate in Palo Alto requires experienced legal, financial, and valuation guidance. Securing an IRS-qualified estate tax appraisal protects beneficiaries, reduces tax risks, and simplifies trust administration.

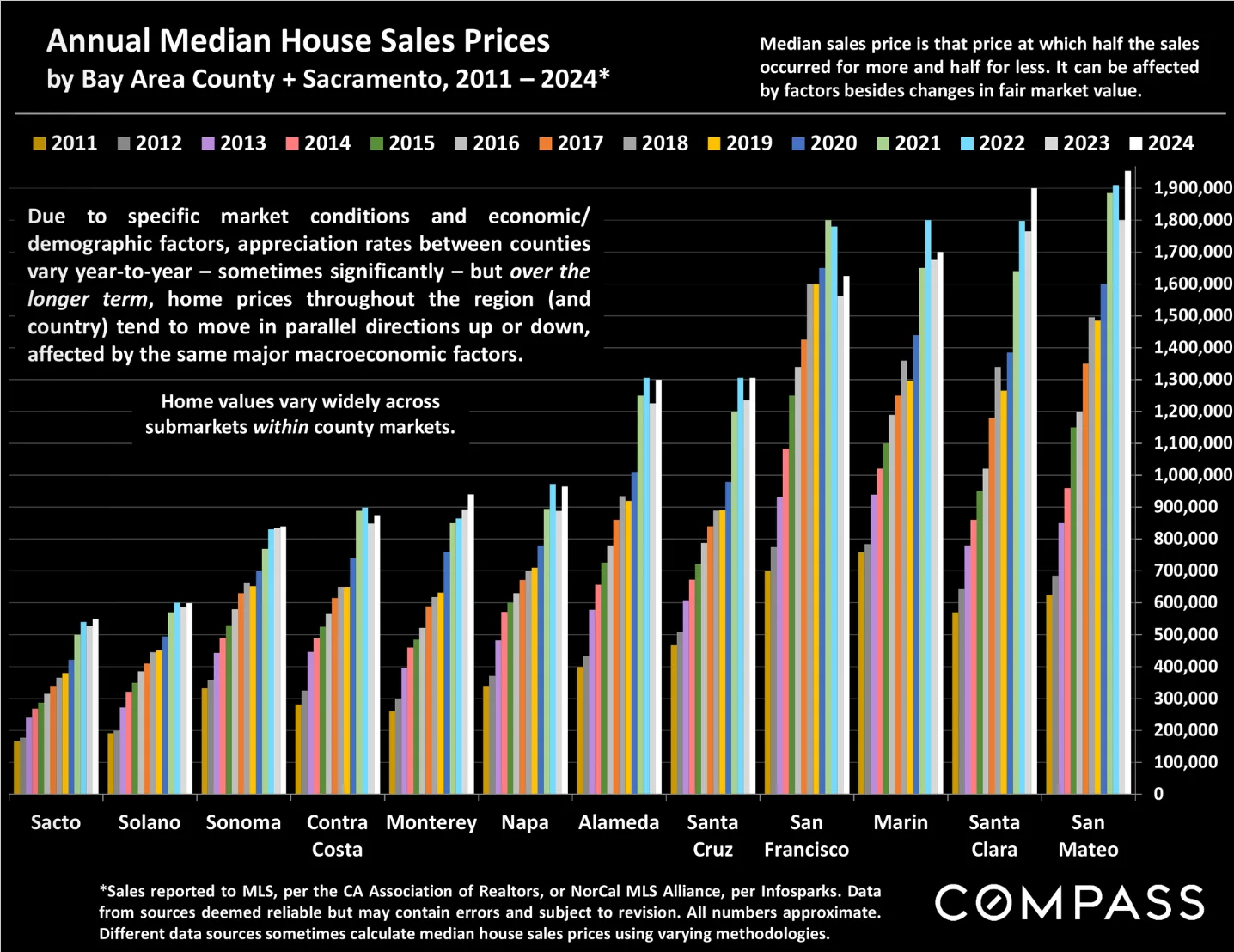

Pacific Appraisers offers broad regional coverage across Northern California, serving clients throughout Santa Cruz, Monterey, San Mateo, and Santa Clara counties.

If you are an estate attorney, trustee, executor, or wealth manager needing an IRS-qualified estate tax valuation in Palo Alto or the surrounding Silicon Valley area, contact Pacific Appraisers today to arrange a confidential consultation.