It’s called the “step-up in basis.” When paired with a professional, local real estate appraisal, it is one of the single most powerful tools available to protect your family’s generational wealth from a massive tax bill.

Because San Francisco Bay Area real estate values have skyrocketed so dramatically over the last few decades, the stakes here are much higher than almost anywhere else in the country. If you plan to leave a Bay Area home to your children, or if you’ve recently inherited one, understanding this rule is critical.

What is a “Basis” and Why Does the Bay Area Care?

In tax terms, your “cost basis” is generally what you originally paid for a property. When you sell a home, you owe capital gains tax on the profit—which is the difference between your selling price and that cost basis.

In many parts of the country, capital gains are relatively modest. But in the Bay Area, where homes bought for five figures a generation ago are now worth millions, the potential tax liability can be staggering.

Fortunately, when a property is passed down through an estate after an owner passes away, the IRS allows the cost basis to “step up” from the original historical purchase price to the fair market value of the home on the exact date of the owner’s death.

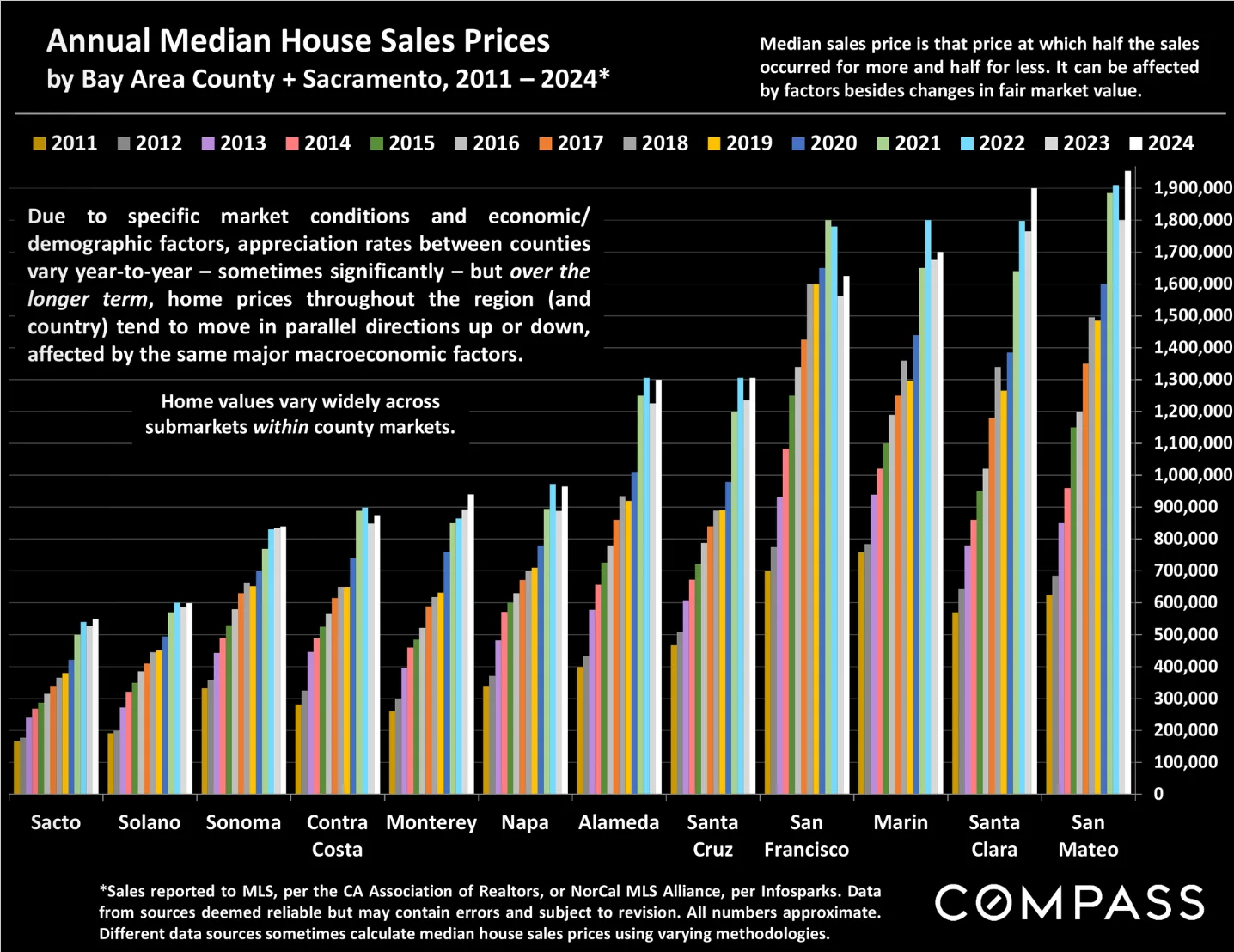

The Bay Area Reality: A Tale of Massive Appreciation

Let’s look at a realistic local example to see how this plays out.

The Scenario:

Imagine your parents bought a classic single-family home in San Francisco’s Sunset District, or a ranch home in San Jose, back in 1980. At the time, the median home price in San Francisco was roughly $130,000.

Fast forward through the dot-com boom, the tech expansion, and the recent AI-driven market surge. By the time the surviving parent passes away, that same home is now worth a median price of $2,000,000.

If you inherit that home and need to sell it to split the proceeds among siblings, here is the difference between selling without a stepped-up basis versus utilizing it:

| Tax Factor | Without Step-Up Basis (If the home was gifted to you before death) | With Step-Up Basis (Inherited upon death) |

| Original Purchase Price (1980) | $130,000 | $130,000 |

| New Tax Basis | $130,000 (Your basis is “carried over”) | $2,000,000 (Stepped up to date-of-death value) |

| Selling Price | $2,000,000 | $2,000,000 |

| Taxable Capital Gain | $1,870,000 | $0 |

| *Estimated Tax Owed (Combined Federal & CA) ** | Approx. $600,000+ | $0 |

*Note: California taxes capital gains as ordinary income, meaning hyper-inflated Bay Area gains easily push heirs into the highest state tax brackets alongside federal taxes.

By inheriting the property at death, the old $130,000 basis is completely erased. Your new baseline is $2,000,000. If you sell the house shortly after inheriting it for that amount, your taxable profit is zero, saving your family over half a million dollars in taxes.

Why a Professional, Local Appraisal is Mandatory

The IRS and the California Franchise Tax Board (FTB) are well aware of how much Bay Area real estate is worth, and they will not accept guesswork when you claim a stepped-up basis. You must legally prove the value via a date of death appraisal (also known as a retrospective appraisal).

- The Problem with Zillow or Redfin: Online algorithms cannot accurately track hyper-local Bay Area micro-markets. An algorithm doesn’t know if a house has sweeping views of the Marin Headlands, whether it has been meticulously renovated, or if it requires $200,000 in seismic retrofitting.

- The Problem with Tax Assessments: Because of Proposition 13, your parents’ property tax assessment was likely locked into a value drastically lower than real-world market conditions. The IRS strictly rejects property tax bills as proof of fair market value.

- The Certified Solution: A certified local appraiser looks backward in time. We analyze historical MLS data, neighborhood-specific trends, and comparable sales matching the exact window of time surrounding your loved one’s passing to establish a bulletproof valuation report that complies with USPAP and IRS standards.

Planning to keep the house? Even if the heirs choose to hold onto the property as a rental or a primary residence, obtaining an appraisal immediately during probate is vital. It locks in that $2,000,000 baseline. If you decide to sell the home 10 years from now when it’s worth $2.5 million, you will only pay capital gains on the $500,000 of growth since the date of death, rather than the entire history of the property.

Protect Your Family’s Hard-Earned Equity

In a real estate climate as highly valued as the San Francisco Bay Area, leaving a property valuation up to chance can result in catastrophic tax penalties or an aggressive audit.

Are you currently settling a local estate or organizing a trust? Let us protect your family’s generational wealth. Contact our experienced team at Pacific Appraisers today for a confidential, IRS-compliant estate valuation consultation.